3 Reasons founders are putting off pitching VCs

3 Reasons founders are putting off pitching VCs

During my time at Bessemer, I noticed a new and growing trend among founders: Raising a first round of venture capital right away is not a priority for them.

The leadership teams at many of today’s startups are putting off the pitch for a number of reasons, three of which I’d like to highlight here:

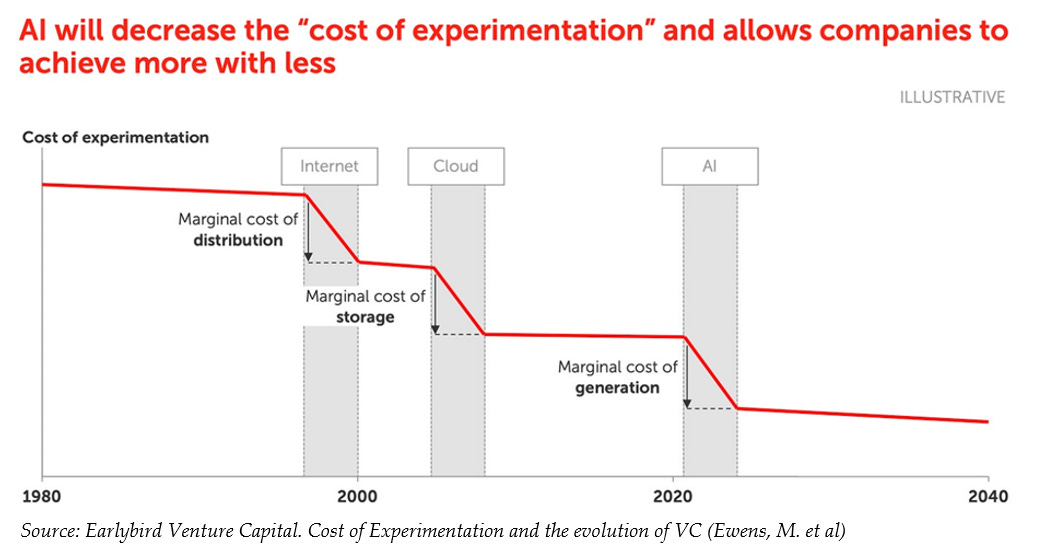

1. The cost of doing business is a lot cheaper than it used to be.

Midjourney, a prominent AI text-to-image generator, is a good example. It scaled to more than $200 million in revenue with no funding and only a handful of employees. How? The cost of experimentation, which I define as the money spent getting a product ready to scale, has plummeted thanks to advances in technology. The internet cut the cost of distribution. The cloud cut the cost of storage and computing. Now, AI is cutting the cost of the entire creative process, from ideation to production, increasing worker productivity at the same time.

I can see this in my own work. In the process of building a MVP (Minimum Viable Product), I’ve been truly surprised at how far and how quickly I can test an idea with existing no/low code platforms and AI-powered software while outsourcing developer work on the cheap. For the time being, I don’t think outside capital will expedite my early-stage goals, and I get the sense that many other founders feel the same way.

With this scaled productivity, I believe we’ll see more and more founders reaching the standard milestones for early rounds (having an MVP, showing indications for PMF, etc.) with less capital and fewer resources, seeking venture funding only when they are ready to scale the product.

2. They want to keep their exit options open.

VC money comes with conditions. For one, you commit to generating a venture-scale return—which is to say, you commit to becoming a unicorn and going public (pretty much). In the early days of a startup, however, it’s near impossible for a founder to know whether or not their company has unicorn potential. By putting off fundraising, they not only have the chance to find out but also the freedom to keep their options open. They might choose to sell their business early, or focus on steady growth or cash-flow generation, which are not things in the VC’s “capital-as-a-strategy” playbook.

Another well-known option for founders (but one still worth highlighting here): retaining control of your day-to-day decisions. Once you’ve taken VC money, they will check in regularly on your progress and expect to be included in any key decisions you make. Founders who want to set their own pace may take a “slow is fast” approach and avoid rushing to take that money.

3. Dilution is just as important as valuation, especially in this down market

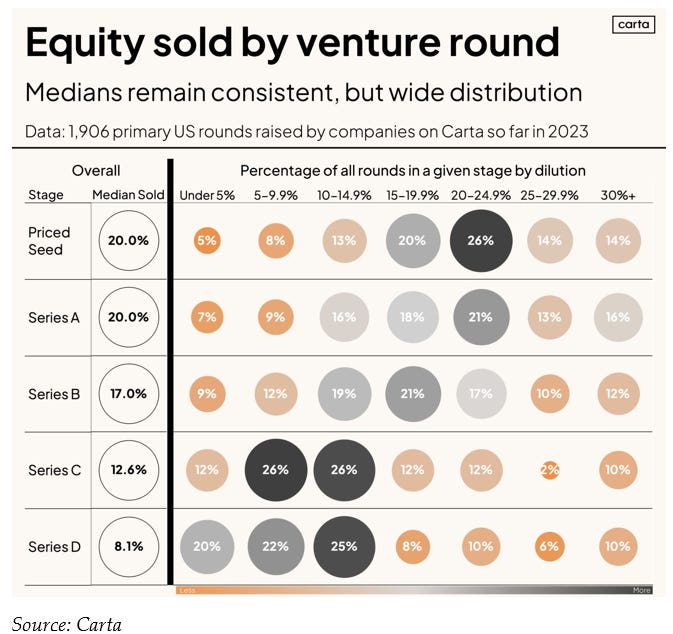

A sky-high valuation and millions in capital raised from a prestigious VC firm are definite dopamine hits. But it’s the money the founding team takes home that keeps them motivated. Every time a new round is raised, everyone in the cap table sees their holdings diluted, especially considering most VCs have ownership targets. According to Carta, a startup on average dilutes 20% in a priced seed round, 20% in Series A, 17% in Series B, and 12.6% in Series C, so raising four rounds already cuts the founder’s ownership in half.

If you factor in the current market and its lower valuations on average, the numbers get worse. The higher the raise against a lower valuation, the greater the loss in value for founders. And that’s not even accounting for the dilutive terms that VCs can sometimes add to a deal, stock compensation to employees, and the likelihood of still more fundraising in the future. So, going back to my first point, a bit of bootstrapping early on could keep dilution to a minimum and retain value for founders.

Raising capital right away is no longer necessary to launch a company. And I’d go so far as to say that being known as a capital-efficient founder will soon rival the bragging rights that come with a big VC investment.